Financial Vulnerabilty

Financial vulnerability is a financial shock created by yourself or other people or events over which you have no control, like losing your job or being diagnosed with a severe illness. This will include loss of income, loss of capital, unexpected expenses and increased costs.

Showing that you are financially vulnerable is extremely hard and it is even braver to expose it so you can understand your financial vulnerability. It is important to understand your financial vulnerability, this will empower you to do something about your financial risks and reduce your financial vulnerability. This would be the first financial step you take so that you can make smart decisions in the financial block.

The four most expensive “D’s” to watch out for:

- Death

- Divorce

- Disability

- Diseae

A huge financial shock combined with making wrong decisions for example during a divorce or separation, can create long-term financial vulnerability that seems to compound not only your money problems but almost everything that is wrong in your life.

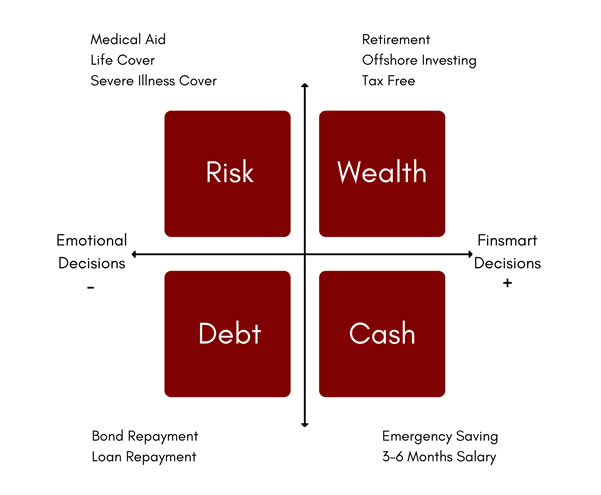

Looking at the financial vulnerability diagram above, always try to stay on the right-hand side of zero especially when making financial decisions. Getting married is big life decision but more importantly a financial decision. In other words stay ‘in the money’, do not take on unnecessary debts and do not increase your risk. An example of increasing your risk is not understanding your marriage contract. A marriage contract in our view is an exit strategy in the event of death, debt (bad debt) or divorce.

When you do your financial planning before and after marriage, move your financial risk as far right as you possibly can. Score as close as possible to +2, then you will eliminate some of the factors that can create financial vulnerability.

Retrenchment, illness, disability or death of a spouse or an ex-spouse are all factors that can trigger financial vulnerability. These are events you can plan for, reducing the risk with smart financial products. The events you can’t really control with financial products are when you get divorced, maintenance payments become an issue; when you have large medical aid co-payments and additional costs for medical procedures; when your children go to high school or university and big non-refundable deposits are required. As you know, often when it rains, it pours.